VAT

As of 1 April 2017 it has been a legal requirement that you must registered for VAT once your turnover for the last consecutive 12 months exceeds £85,000. However you may choose to voluntarily register for VAT before your turnover reaches this figure.

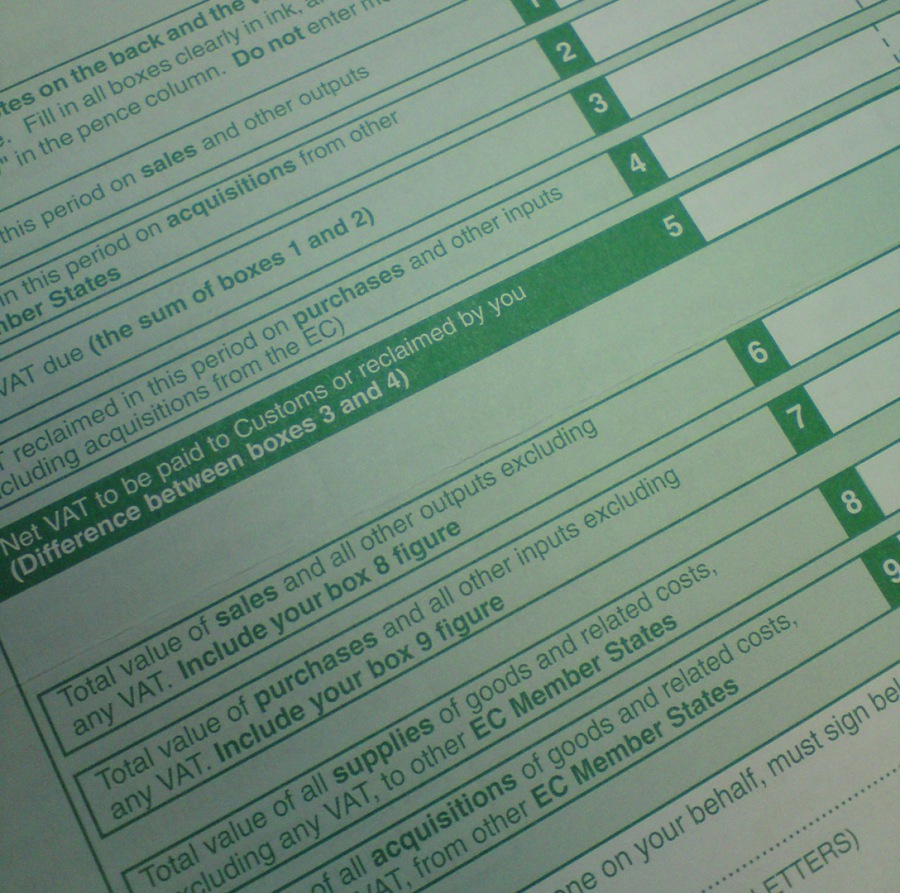

If your business is registered for VAT you will need to complete a VAT Return and send it to HM Revenue & Customs, usually on a quarterly basis (i.e. every 3 months) along with any payment of VAT that is due.

The Book Monitor can calculate how much VAT your business needs to pay and complete the VAT returns on your behalf. Ideally this should be done using cloud accounting software, so that your VAT return can be filed directly with HMRC. We are also able to prepare your VAT return if you are using the flat rate VAT scheme or the annual accounting scheme and can advise you on whether or not either of these schemes would be beneficial to your business.

Frequently Asked Questions:

Q: What is the standard rate of VAT?

A: Since 4 January 2011 the current standard rate of VAT, has been 20%. Between 1 January 2010 to 3 January 2011 the standard rate of VAT was 17.5%. Between 1 December 2008 to 31 December 2009 the standard rate of VAT was temporarily reduced to 15%. Before 1 December 2008 the standard rate of VAT was 17.5%.

Q: When is it compulsory for me to register for VAT?

A: As of 1 April 2017, once your turnover has exceeded £85,000 in the previous 12 months (this is calculated on a rolling basis, meaning you need to add up your total income for the last 12 months at the end of every month) you must register for VAT.

Q: Can I register for VAT before my turnover has reached £85,000?

A: Yes, you can voluntarily register for VAT at any time. It only becomes compulsory to register for VAT once your turnover has exceeded £85,000.

Q: What is the Flat Rate Scheme turnover limit?

A: The turnover limit for using the Flat Rate Scheme for VAT is £150,000 per annum.

Q: What is the Annual Accounting Scheme?

A: The Annual Accounting Scheme allows you to file one VAT return a year, on an annual basis.

Q: What is the Annual Accounting Scheme turnover limit?

A: The turnover limit for using the Annual Accounting Scheme for VAT is £1,350,000 per annum.

Q: Can I deregister for VAT?

A: If your business is closing down or your turnover has reduced (and you believe will remain below the VAT deregistration threshold for the foreseeable future) you may decide you want to deregistered for VAT. You can only deregister once your turnover has dropped below £83,000 in the previous 12 months or when your business is finally closed or ceases to trade.

Contact us today!

If you would like more information or wish to make an appointment please contact us:

T: 07795 832597

E: info@thebookmonitor.co.uk

or use the Contact Us page.

Useful Links